Pluxee NV (PLX)

French employee benefits company spin-off

Employee Benefits sector

Employee benefits are compensation packages that include extras such as food and meals vouchers, health insurance, retirement savings plans, paid vacation days and more. Employers offer employee benefits to attract and retain top talent, as well as improve employee productivity and engagement. These are important because studies have shown that employees who feel valued and appreciated by their employer are more likely to stay with the company and be productive. Some benefits are even required by law and they do often have favourable tax implications.

The sector has been suffering some headwinds during the year caused by regulatory discussions/ changes in France and most recently in Italy. These changes could limit the profitability of the sector but their impact has been exaggerated in our opinion.

Company Description

Sodexo spin-off Pluxee N.V. provides employee benefits and engagement solutions services in France, Latin America, Continental Europe, and the rest of the world. The company offers employee benefits comprising meal, food, gift, mobility, training, and wellness benefits; and other products and services, including rewards and recognition, public benefits, and fuel and fleet management.

The company has existed as a Sodexo Benefits and Rewards since 1976 which has allowed Pluxee to position itself as the leader in the segment in 17 countries. Company’s revenues are divided into two dimensions from which to become the client’s trusted HR partner:

Employee benefits: meal and food benefits and lifestyle benefits making about 80% of revenues.

Other products and services: employee engagement and reward recognition, Pluxee offers through its app access to discounts and auxiliary services acting as a marketplace for employees.

Pluxee offers a good app interface with much more flexibility for employees and HR departments to manage all company benefits. By centralising all information and billing related to employee benefits in a single report, Pluxee makes it easy for HR to provide these services, which help to retain talent - a key concern for companies nowadays. The user experience of the app is much better than competition (Edenred) as can be seen in AppStore/Google Play reviews. This is very important, a good app translates into a greater consumer engagement, which translates into more commissions for Pluxee.

Pluxee’s value lies on their efficient tax benefit management. Any company can issue a preload card so employees spend their money daily on food, but managing tax related spending is a different story. The need for tax management expertise and an extensive network is a major barrier to entry, helping to prevent the entry of new players who would accept lower margins and therefore lower Pluxee's margins.

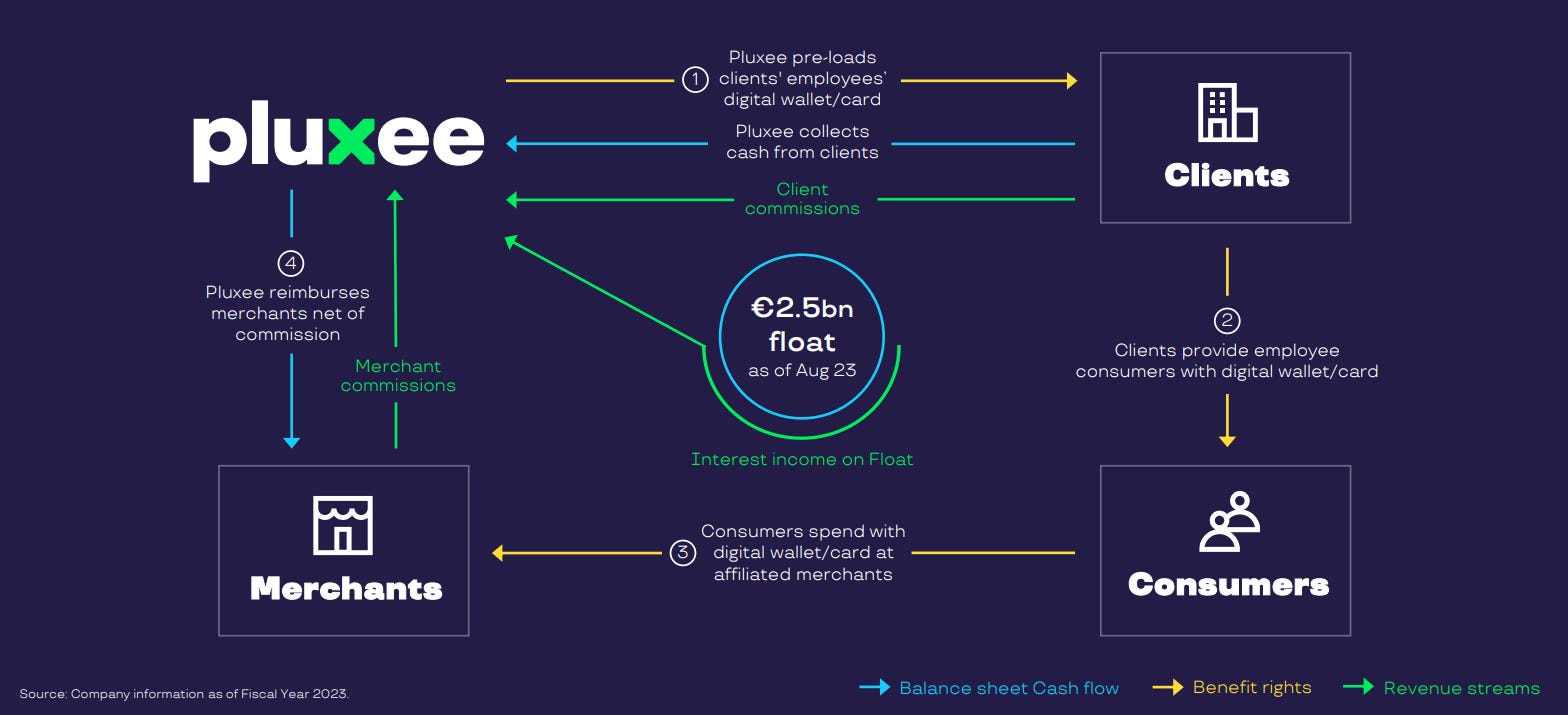

Cash flow generation and profitability

Pluxee business model obliges clients to finance its operations which converts the company into a cash generative machine and allows for almost free scalability. Here is how this business model works over time:

Cash Collection. Pluxee collects cash from the clients (companies) in exchange for a loaded digital wallet/card.

Client Distribution. Clients provide consumers (employees) with those wallets/cards so they can spend the loaded money in the affiliated merchants.

Merchant Reimbursement. Pluxee reimburses merchants net of commission.

Pluxee earns money in three different ways throughout this process:

Commissions on Clients. Pluxee earns commissions from loading client employees wallets/ cards. These commissions tend to be low (under 1%) and they are usually lower in big corporate clients than in SME clients.

Commissions on Merchants. Pluxee charges merchants a commission of around 5% on every purchase made with a Pluxee card. This generates more than 50% of the total revenue.

Interest on the Float. As clients pay Pluxee at the beginning of this period and Pluxee pays merchants at the end of this period, Pluxee can invest this money, the so-called float, and earn interest income on it.

The structure shown above is reflected in its financial statements where:

The company has generated 88% cash flow conversion in FY2024, expects a 75% conversion for 2025, 2026 on what could be considered conservative estimates

The growing amount of "value in circulation and related payables," which is the amount loaded onto cards that have not yet been used and amounts owed to affiliated merchants.

The company has achieved a 35% EBITDA margin in 2024 and raise it to 37% EBITDA margin in FY2026. It is important to note that FY2024 operating profit has been affected by 45 million one-off charges related to the spin-off.

Growth

Pluxee management is targeting low double digit organic growth during FY 2025 and 2026. This guidance was considered conservative in the 3Q Earnings call by some analysts taking into account that the company has over achieved its growth objective for FY 2024 to 18.6% from 15% set out initially.

We believe that management is not being aggressive with guidance in order to manage expectations but there are many drivers that could help the company to reach growth above 15%:

Santander partnership in Brazil: only 20% of SMEs in Brazil use Meal and Food benefits, the partnership with Santander will allow Pluxee to reach up to 1.4 million of Santander customers. Edenred performed a similar strategy by collaborating with Itaú which has resulted in growth above 15% over the last 3-4 years. The effect of the Santander collaboration will start reflecting in Pluxee’s financial statements during FY 2025. Pluxee should achieve a high teen level of revenue growth in Brazil which currently represents 12% of revenue.

Inflation effect: the business model is a inflation beneficiary as governments should adjust the acceptable face value of the benefits that employees can receive. This effect always comes with a lag and even though some countries have already increased their limits there are still many others which have not seen updates in the acceptable amount. Pluxee will benefit from these changes as it increases the total transaction volume.

Digitalization: historically Food and Meals benefits in many companies were provided through paper cheques. The market is now shifting to a fully digital offer which not only brings cost efficiencies but facilitates the usage of the benefit increasing the transaction volume. Moreover, having a digital platform from which to reach employees makes it easier to grow revenue from auxiliary products in the “Other products and services” category. There are multiple tailwinds pushing for digitalization even in well established markets, for example, the French government's regulatory focus has shifted more towards the "modernization" of the meal benefit system which is aligned with Pluxee’s strategy and interests.

In terms of inorganic growth, management has stated its ambition to make acquisitions and has realised its first with "Cobee", a start-up competitor with a presence in Spain and Portugal. Details about the transaction are still pending but in terms of business quality Cobee was well recognised in the Spanish environment and had an extensive client base. Effects of the transaction will be neutral on financial statements until FY 2026. However, we would like to see the multiples paid in this transaction in order to check how disciplined management is going to be on its inorganic growth strategy.

Management and Owners

Being a family business is a significant advantage (the Bellon family holds ~43%), as investors like Warren Buffet and Francisco García Paramés have noted several times. Both also coincide on the advantages of letting a good management run the company when they have demonstrated reliability.

Pluxee’s CEO has extensive experience in running this type of business, having led this part of the company since 2017 while at Sodexo. Now, as an independent entity, he is free to develop his plans without constraints, aligning his interests with those of the company's owners. His career is now deeply tied to the company's success.

Management compensation is linked to achieving objectives, which would lead to a fair development of the company. These objectives have been updated, demonstrating confidence from management of the growth prospects of the company.

The family ownership structure of Pluxee ensures that shareholders will be rewarded, as the family members themselves have interest in the company's success and returns to the shareholders. With their experience in managerial positions and ownership of their own company, they have a great understanding of the business and are committed to creating value for shareholders, which is where this spin off comes from. The company's history with Sodexo demonstrates a strong commitment to returning value to shareholders without compromising growth through dilution. Additionally, Pluxee have already made a stock buyback program and has already committed to distributing 25% of its earnings as dividends from FY 2024 onwards.

Risks

There are several important risks to consider:

Regulatory risk. Pluxee’s income is heavily reliant on tax benefits, changes in those regulations could harm revenue and margins. An example of this is Italy’s new law, which imposes a 5% cap on merchants' fees for meal vouchers in the private sector. Pluxee is already in that range so it wouldn’t hurt their margins much as long as the regulation does not become stricter. However, Pluxee can justify the charges as this process requires a vast network of business, expense data management and tax regulation. Additionally, governments prioritise preventing tax evasion and fraud, so it makes them more likely to accept reasonable commissions in exchange for secure and trustworthy operations.

Economic Risk. Any economic scenario where spending is reduced or employees are laid off would affect Pluxee negatively. Nevertheless, Pluxee is covered against these scenarios by 2 main reasons:

Firstly, the meal and food benefits offer a valuable solution for individuals who still need to eat out, even in times of economic uncertainty. The end user is saving an average of 30% when using the benefits compared to spending his salary which is a strong motivation to maintain them. People will still want to eat out, if they have this product, they will use-up their tax free credit first.

Secondly, Pluxee has a diversified global presence, with 45% of its income generated in Continental Europe, 38% in Latin America and 17% from other regions. Consequently, unless a global crisis occurs, Pluxee is well-positioned to navigate local market challenges.

Interest Rates Risk. A lower interest environment would reduce profit from float. However, a decline to negative interest rates, as 3 years ago is unlikely as markets are predicting. In that case, inflation would surge and countries should respond by adjusting tax benefits, which Pluxee would benefit from as commented previously.

Competition Risk. New entrants in the industry that are willing to accept lower margins would harm Pluxee’s margins, but they have some barriers to entry to get through first. On one hand, you need an extensive network of restaurants in order to be attractive to clients, on the other hand you need expertise and technology to implement the efficient tax related spending. Even though Pluxee is a new brand, it already has a moat from their long journey as part of Sodexo. Additionally, when there isn’t much to save, companies will prioritise security and reliability over a small saving cost, it is the kind of product that people will stick with unless something goes wrong.

Valuation

The sector is currently being valued very negatively specially after some negative regulatory news in Italy in the last weeks. Given the lower importance of Italy for Pluxee we see the recent drop in the share price as a great opportunity to get this business at a good fair price. Nevertheless, we believe that Edenred and Pluxee are two companies with a sustainable growth runway and a capital-efficient business model and they should not trade at 6x EV/EBITDA. Both companies are targeting low double digit growth over the following years which we believe is a conservative estimate in the case of Pluxee and more aggressive from Edenred given its size and penetration in many markets.

Looking at the Company on a “FCF yield + growth” basis. At a ~460 m € projected recurring free cash flow for 2024 (19% 2024 FCF yield) (which includes slightly elevated investment in technology to “catch up” to Edenred) for a company growing its FCF at a mid-teens rate implies over ~30% IRR over the next few years. Given the growth profile, attractive business characteristics, and strong moat of this business, we think that the market is not fairly valuing the Company.

Investment thesis

Pluxee's recent spin-off process has created an investment opportunity in a growing, high-margin sector at a discount. Given growth and margin expectations, Pluxee’s valuation remains low. Pluxee is also partially hedged against the various risks that should occur, making it a relatively secure investment. The cash flow generation and light capital model that characterises companies in the sector allows them to reward shareholders in a way that other heavy capital companies are not able, and the significant barriers to entry protect their margins against new entrants. In addition, management is well incentivised and the Bellon family, the majority shareholders, are on hand to ensure the right return to the shareholders.